In the first half of 2014 five office buildings were delivered, with a total rentable area of 68,500 sq. m. Approximately 66% have been completed in Q2. At the end of H1 2014 Bucharest’s modern office stock reached 2.114 million sq. m. By the end of the year we expect another 63,500 sq. m of new supply in office projects such as Green Court I, AFI Business Park III, Ethos House or City Offices.

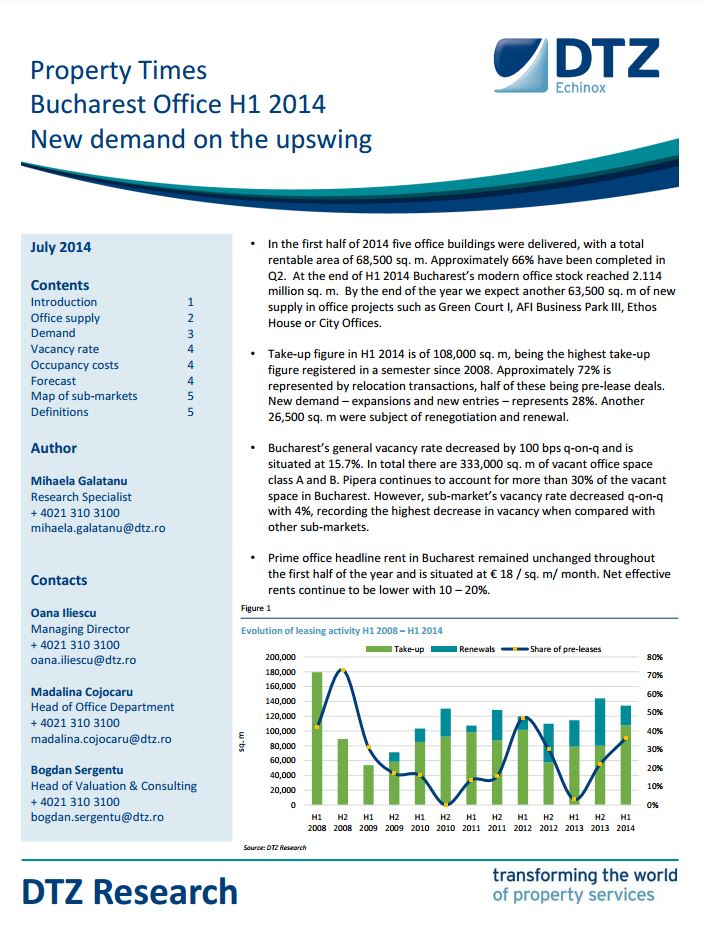

Take-up figure in H1 2014 is of 108,000 sq. m, being the highest take-up figure registered in a semester since 2008. Approximately 72% is represented by relocation transactions, half of these being pre-lease deals. New demand – expansions and new entries – represents 28%. Another 26,500 sq. m were subject of renegotiation and renewal.

Bucharest’s general vacancy rate decreased by 100 bps q-on-q and is situated at 15.7%. In total there are 333,000 sq. m of vacant office space class A and B. Pipera continues to account for more than 30% of the vacant space in Bucharest. However, sub-market’s vacancy rate decreased q-on-q with 4%, recording the highest decrease in vacancy when compared with other sub-markets.

Prime office headline rent in Bucharest remained unchanged throughout the first half of the year and is situated at € 18 / sq. m/ month. Net effective rents continue to be lower with 10 – 20%.

Your search results