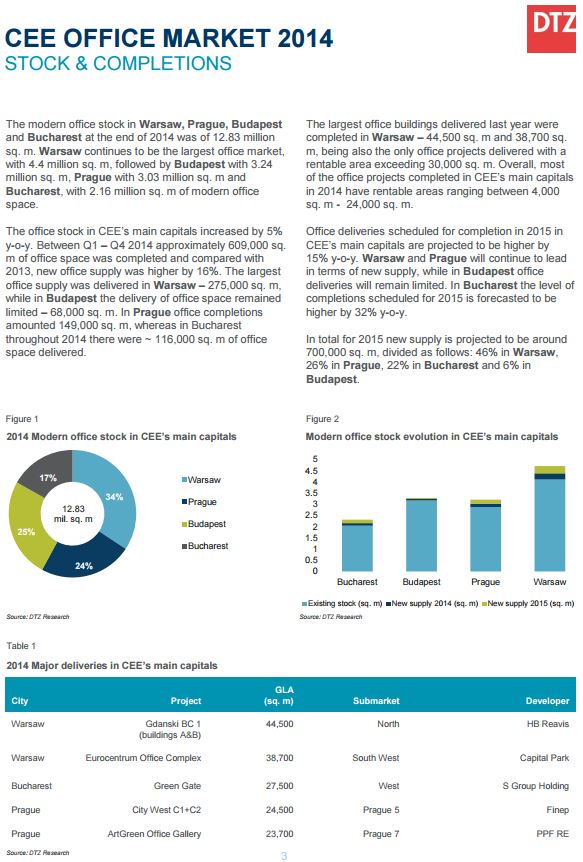

The modern office stock in Warsaw, Prague, Budapest and Bucharest at the end of 2014 was of 12.83 million sq. m. Warsaw continues to be the largest office market, with 4.4 million sq. m, followed by Budapest with 3.24 million sq. m, Prague with 3.03 million sq. m and Bucharest, with 2.16 million sq. m of modern office space.

The office stock in CEE’s main capitals increased by 5% y-o-y. Between Q1 – Q4 2014 approximately 609,000 sq. m of office space was completed and compared with 2013, new office supply was higher by 16%. The largest office supply was delivered in Warsaw – 275,000 sq. m, while in Budapest the delivery of office space remained limited – 68,000 sq. m. In Prague office completions amounted 149,000 sq. m, whereas in Bucharest throughout 2014 there were ~ 116,000 sq. m of office space delivered.

The largest office buildings delivered last year were completed in Warsaw – 44,500 sq. m and 38,700 sq. m, being also the only office projects delivered with a rentable area exceeding 30,000 sq. m. Overall, most of the office projects completed in CEE’s main capitals in 2014 have rentable areas ranging between 4,000 sq. m – 24,000 sq. m.

Office deliveries scheduled for completion in 2015 in CEE’s main capitals are projected to be higher by 15% y-o-y. Warsaw and Prague will continue to lead in terms of new supply, while in Budapest office deliveries will remain limited. In Bucharest the level of completions scheduled for 2015 is forecasted to be higher by 32% y-o-y. In total for 2015 new supply is projected to be around 700,000 sq. m, divided as follows: 46% in Warsaw, 26% in Prague, 22% in Bucharest and 6% in Budapest.