Throughout the first three quarters of 2014, Bucharest office market has registered positive evolutions. The pre-lease activity has demonstrated consistency, new demand’s share in total take-up has gained importance and the rental level continued to be considered attractive by most office occupiers .

As a direct consequence, during Q1 – Q3 2014, the general vacancy rate for class A & B office space has decreased from 16.7% to 14.5%. More than that, during the 3rd quarter of 2014, the vacancy rate has fallen in all sub-markets. Finding Bucharest’s office market conditions interesting, developers are already announcing new projects. Most of them are investors with a proven track record in delivering office projects in Bucharest, are familiar with the needs of the office occupiers and thus have the experience and the knowledge necessary in order to attract tenant’s interest towards new office projects.

Currently under construction with an estimated delivery date for the next two years are 166,000 sq. m. Additionally, more than 500,000 sq. m of office space located all over Bucharest are in different stages of planning. However, only projects with a solid pre-lease agreement in place are likely to get financing.

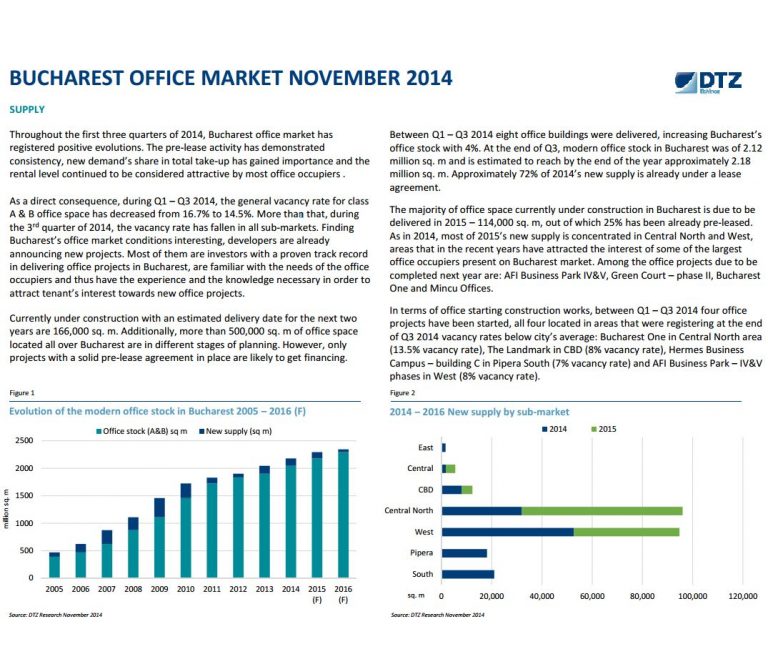

Between Q1 – Q3 2014 eight office buildings were delivered, increasing Bucharest’s office stock with 4%. At the end of Q3, modern office stock in Bucharest was of 2.12 million sq. m and is estimated to reach by the end of the year approximately 2.18 million sq. m. Approximately 72% of 2014’s new supply is already under a lease agreement.

The majority of office space currently under construction in Bucharest is due to be delivered in 2015 – 114,000 sq. m, out of which 25% has been already pre-leased. As in 2014, most of 2015’s new supply is concentrated in Central North and West, areas that in the recent years have attracted the interest of some of the largest office occupiers present on Bucharest market. Among the office projects due to be completed next year are: AFI Business Park IV&V, Green Court – phase II, Bucharest One and Mincu Offices.

In terms of office starting construction works, between Q1 – Q3 2014 four office projects have been started, all four located in areas that were registering at the end of Q3 2014 vacancy rates below city’s average: Bucharest One in Central North area (13.5% vacancy rate), The Landmark in CBD (8% vacancy rate), Hermes Business Campus – building C in Pipera South (7% vacancy rate) and AFI Business Park – IV&V phases in West (8% vacancy rate).